Policy & Practice for Purposeful Business

The final report of the Future of the Corporation programme

By The British Academy

Download report

- Published by

- The British Academy

- Year

- 2021

- ISBN

- 978-0-85672-669-9

- Pages

- 62

Policy & Practice for Purposeful Business

Download reportForeword

In 2016, when the idea for the British Academy’s programme to examine the role of business in society was first discussed, no-one could have anticipated the pace of change we would all face in the following years. The programme had already been highlighting the growing crisis linked to climate change. Months after the publication of its second report, Principles for Purposeful Business, COVID-19 exposed the world’s vulnerability to a second collective crisis, a global pandemic. As society looks to recover from the pandemic and to mitigate climate change, business can and must play a positive role in creating a fairer, more resilient future.

This final report goes further than any other towards explaining both how business can do this by changing its practices and how public policy can enable and promote these changes. The findings in the report bring together the results of four years of in-depth research and extensive engagement with hundreds of business leaders, researchers, policymakers and other practitioners.

The programme has harnessed the breadth and depth of ideas and expertise from right across the SHAPE disciplines (Social Sciences, Humanities and the Arts) ranging from Law, Economics and Business and Management Studies to Philosophy, Languages and Medieval History. As the national academy for these subjects, we have been ideally placed to host such a programme and convene academia, business and civil society.

We believe the Future of the Corporation programme is the most extensive review of the ways in which corporate purpose can be placed at the heart of business. Change will require collective action and a system wide shift, with multiple people and businesses working together. This report sets out a range of pathways to help us get there. We urge those committed to putting purpose at the heart of business to make use of the huge range and depth of ideas laid out in this report to bring about that change.

Professor Julia Black CBE

President of the British Academy

Executive Summary

Since 2017, the Future of the Corporation programme has been exploring the role of business in society. The programme builds on a long tradition of championing the remarkable growth, prosperity and poverty alleviation that business has generated on the back of its creativity, entrepreneurship and innovation. At the same time, we have not shied away from acknowledging the negative impacts that some businesses and business models have had. Now at its conclusion, the programme has clarified the potential for business to address problems of people and planet, and this report sets out that vision and a framework of policy and practice for achieving it.

Exploring the role of business in society means going well beyond the challenges of individual businesses or sectors. Society is still in the grip of an unprecedented global pandemic which continues to have dramatic effects on social, economic and cultural life as described in the British Academy’s landmark COVID Decade report. No less urgent are the climate emergency, climate impacts, biodiversity loss, inequality, social exclusion, the technological revolution, the future of work and other global challenges we face. Fully engaging business in these challenges will not happen automatically, and business policy and practice retains many of the features that have led it to focus mainly on financial goals and not on solving the problems of people and planet.

This report argues for a coherent package of changes to policy and practice that together support the implementation of corporate purposes and hold decision-makers to account for them. We have found over four years of research, engagement, polling and collaboration with other initiatives that there is a growing appetite for purposeful business, including from business itself, investors, policymakers, regulators, employees, consumers and other stakeholders. We use the term “purposeful business” to summarise a system in which the purpose of business is creating profitable solutions for problems of people and planet, and not profiting from creating problems.

A permissive legal, regulatory, governance and reporting framework is required to enable and encourage purposeful business, and the UK has such a framework. But in the UK there is insufficient accountability for, and implementation of, purposeful business. Few companies take up the option that exists within the law to adopt purposes beyond promoting shareholder interests, and there is insufficient appreciation and enforcement of directors’ duties under the law. Internationally, initiatives are currently in progress to ensure that companies and investors report their environmental and social impacts, but there has been insufficient focus on measuring, valuing and incentivising corporate purpose.

With a supportive legal, regulatory, governance and reporting framework in place, there are two mechanisms that together are required to deliver coherent reform:

- Accountability: using the legal, regulatory, governance and reporting framework to hold companies to account for complying with corporate purposes of profitably solving problems of people and planet and not profiting from creating them; and,

- Implementation: ownership, measurement, finance, innovation and investment through which people harness the potential of markets to deliver profitable solutions which benefit customers, the workforce, investors, communities, society and the environment.

To strengthen accountability for corporate purpose, we recommend that:

- governments put purpose at the heart of company law and the fiduciary responsibility of directors.

- regulators are given new powers to hold directors and controlling owners to account for their corporate purposes. Regulators responsible for particular business sectors that provide public functions require utilities, banks, and other licensed companies they oversee to adopt purposes which align with their public interests and engage with their stakeholders about them.

- companies place purpose at the heart of their annual reporting and demonstrate to their stakeholders how their ownership, governance, strategy, values, cultures, engagement, measurement, incentives, financing and resource allocation deliver it.

- investors engage with companies about the nature and implementation of their purposes, and evaluate their performance and future prospects against them.

But reforming business involves more than accountability and compliance with law, regulation, governance and reporting. It is also about the values, commitment, culture, and cooperation of people who implement corporate purpose. Strong ownership and inspiring leadership of purpose are crucial in building close relations between institutions and companies to finance entrepreneurship, innovation and investment in purposeful businesses. Such leadership puts purpose at the heart of companies’ governance, measurement, valuations and incentives, and forges common purposes between business and government to solve local, national and global challenges.

To promote more effective implementation of corporate purposes, we recommend that:

- companies identify long-term committed holders of blocks of their shares. They develop internal values, cultures and systems of measurement and incentives that encourage embedded ownership of purpose throughout their organisations.

- investors develop the expertise required to support long-term financing of small, local as well as large, global purposeful businesses. They promote measurement and reporting of company purposes and ensure that required systems of data and information are available to evaluate company performance against them.

- regulators address impediments that may exist to companies having long-term committed shareholders. They encourage international standard setters to promote systems of measurement and accounting for company purposes and ensure that financial reports reflect the costs and profits of delivering them.

- governments, companies, and non-governmental organisations co-invest in partnerships based on common purpose around tackling issues such as inequality, social exclusion, climate change, biodiversity loss and the future of work.

This report builds on the eight Principles for Purposeful Business described in the previous Future of the Corporation report, covering law, regulation, ownership, governance, measurement, performance, finance and investment, and proposing changes that are led by government, regulators, business, and investors. It is based on an extensive process of research, deliberation and engagement over the four years of the programme and in particular over the past year during which more than a hundred stakeholders from across the corporate, government, regulatory, civil society and investor sectors debated and scrutinised a detailed set of proposals for policy and practice.

The report returns to the origins of the programme in meeting the challenges of the 21st century by putting people at the heart of business. We draw a clear link between policies and practices that enable and encourage purposeful business and the potential for business to work in collaboration with governments, investors and regulators in addressing the challenges we face. We describe how business can do this in relation to net zero and a “just transition”; economic and social recovery from COVID-19; reduced inequality, social exclusion and regional disparities; and technological innovations that enhance the future of work. We conclude with a call to each and every one of us to use our voice and influence as consumer, employee, investor and citizen to assist with putting purpose at the heart of business.

Introduction

The question this report addresses is how business, investors, governments and regulators can create an enabling and encouraging environment for purposeful business as set out in the Future of the Corporation programme.

The Future of the Corporation programme was described by the Financial Times as one of the world’s most ambitious efforts to reform capitalism for the 21st century. (1) It has made the most of the British Academy’s considerable reach among academia, policymaking, business and civil society, drawing on academic research across the Social Sciences, Humanities and Arts for People and the Economy (SHAPE) (2), and the insight of hundreds of experts who have generously given their time over the four years it has operated. This report is the result of that process.

The report reflects an appetite for change. A survey (3) carried out in 2020 by YouGov for the Future of the Corporation programme revealed that 44% of business leaders agreed with the British Academy’s definition that the purpose of business was to “find profitable solutions to the problems of people and planet, not to profit from creating problems for either.” It also highlighted that just 15% of the senior decision-makers in business thought that the current legal and regulatory environment served society’s – rather than shareholders’ – interests. Furthermore, almost two thirds (63%) of those surveyed reported taking steps to make their own businesses more purposeful. Similarly, a recent Institute of Directors survey of over 700 directors found that 62% believed that businesses should not exist solely to make money and generate shareholder profits, while half felt that companies should have a stated social purpose to help solve problems in society. (4)

While the findings and proposals are particularly pertinent to the challenges that large companies confront in changing their practices, they are intended to be relevant to all companies – small, medium and large, publicly listed and privately owned, entrepreneurial start-ups and social enterprises – and, although reference is frequently made to companies and policies in the UK, the insights of the report can be applicable to companies and countries around the world.

This introduction summarises the two previous publications that laid the foundations and the methodology of the programme. The second section sets out the vision for purposeful business that delivers economic prosperity, social justice, and environmental sustainability.

The third section puts forward proposals for realising that vision. It describes public policies and business practices needed to enable and encourage purposeful business:

- For policymakers, regulators and their officials, it provides a basis for comprehensive design of accountability mechanisms for purposeful business.

- For business leaders and investors, it describes how the business environment can enable and encourage implementation of purposeful businesses.

- For researchers and policy advisors, it establishes a framework and criteria by which business practices and public policies towards business can be evaluated.

The fourth section illustrates how purposeful business can assist with enhancing economic, social and environmental wellbeing by solving major, complex problems.

The report cites examples – described as starting points – of public policy, and business practice initiatives that are currently in progress. They are included as illustrations of the issues raised in the report, but it is important to appreciate that no single company or jurisdiction fully reflects the practices and policies we propose. The examples given should not be viewed as models of best practice without deficiencies or limitations and many other examples and initiatives can be found in other publications. (5)

21st century challenges

Throughout the report we refer to the problems or challenges that face people and planet. The Future of the Corporation programme has explored these in different ways and the British Academy’s recent COVID decade reports, the UN Sustainable Development Goals, World Economic Forum global risk reports, and many others provide different ways to describe the issues. For this report, we have selected four critical challenges, discussed in section 4, to which policymakers are actively seeking solutions and for which business must be part of the answer. We hope that others will extend this analysis to other issues and we leave the agenda open for further research exploring the potential of purposeful business.

Reforming Business for the 21st century

In January 2018, the British Academy established the Future of the Corporation programme to consider the relationship between business and society. It has explored the growing environmental, social and political challenges which business faces and how it can best take advantage of recent technological advances for the benefit of society as a whole.

In November 2018, the programme produced its first report entitled Reforming Business for the 21st Century. (6) The report described what looked at the time to be an ambitious programme of reform of business around its corporate purpose. It suggested a move away from the conventional notion of corporate purpose as being about furthering the interest of shareholders to one that recognised the role of business in addressing the challenges we face as individuals, societies and the natural world in the 21st century.

It emphasised the need for business to address these challenges in a form that is commercially viable, profitable and financially sustainable, while avoiding profiting from causing detriments to other stakeholders. It therefore argued that the purpose of business is to create profitable solutions for the problems of people and planet. In the process it produces profits, but profits are not per se the purpose of corporations.

Principles for Purposeful Business

In November 2019, the British Academy produced a second report setting out eight Principles for Purposeful Business (7):

- Corporate law should place purpose at the heart of the corporation and require directors to state their purposes and demonstrate commitment to them.

- Regulation should expect particularly high duties of engagement, loyalty and care on the part of directors of companies to public interests where they perform important public functions.

- Ownership should recognise obligations of shareholders and engage them in supporting corporate purposes as well as in their rights to derive financial benefit.

- Corporate governance should align managerial interests with companies’ purposes and establish accountability to a range of stakeholders through appropriate board structures. They should determine a set of values necessary to deliver purpose, embedded in their company culture.

- Measurement should recognise impacts and investment by companies in their workers, societies and natural assets both within and outside the firm.

- Performance should be measured against fulfilment of corporate purposes and profits measured net of the costs of achieving them.

- Corporate financing should be of a form and duration that allows companies to fund more engaged and long-term investment in their purposes.

- Corporate investment should be made in partnership with private, public and not-for-profit organisations that contribute towards the fulfilment of corporate purposes.

This set of principles provided a description of how a system that enables and encourages purposeful business could operate. This report builds on that by describing the business practices and public policies required to deliver purposeful business and the potential for purposeful business to solve the global challenges of the 21st century.

Methodology

The findings described in this report are the product of four years of extensive work, involving a substantial body of research and active engagement with a broad range of stakeholders, including those at the most senior levels of business and government. All of this material is publicly available. (8) The programme has used an iterative, cumulative methodology where each step has built on the last, responding to policy and practice developments and drawing on the work of others. Reports from each phase include more detailed descriptions of the respective methodologies at that stage.

The findings presented in this report are derived from this significant base of evidence, illustrated by the key milestones below, which we will refer to throughout:

Phase 1:

- Publication of 13 research papers responding to 10 questions regarding the essential nature, history, and future of business. (9)

- Development of an initial review of findings (‘Reforming Business for the 21st Century’) based on the research, and engagement of business leaders in a series of interviews and events.

Phase 2:

- Publication of a further four research papers exploring some of the levers of change identified in the first phase. (10)

- A series of 16 deliberative roundtables that brought together experts to develop the principles.

- Development of a second review of findings (‘Principles for Purposeful Business’) that put forward a framework for promoting business purpose.

Phase 3:

- Extensive global and public debate in a series of high-profile Purpose Summits involving business leaders, investors, civil society leaders, politicians, regulators and academics in discussions about the findings of the programme. (11)

- A collaborative policy research process (policy labs) engaging over 100 stakeholders across different sectors, exploring options for policy and practice proposals in the UK. (12)

- Assembling examples of policies and practices that illustrate aspects of the proposals. (13)

In all, the programme has produced 17 academic papers involving more than 40 researchers, it has engaged over 200 experts in 29 deliberative, evidence-generating roundtables, and convened over 100 stakeholders in eight policy labs. It has also drawn together thousands who joined the public events. It has been led by a group of well- informed leaders from business, academia, civil society and policymaking through its advisory group who have contributed their insight and knowledge of business practices.

Finally, the findings build on extensive collaborations with other organisations, research groups and business initiatives that have provided additional evidence and insight. (14)

The distinctive approach of this programme has been to provide a comprehensive analysis of the role of business in contemporary society. Instead of examining individual parts of the system, which others have done very effectively, this programme has sought to draw on the collective insight of hundreds of experts and existing initiatives as well as new research to identify the policies and practices that are required to bring about reform.

Vision: what are we aiming for?

Business is continually evolving. History has shown how it adapts to provide new solutions to problems, modifying its form in response to the changing world around it. (15) It has, as a result, been a remarkable source of economic prosperity and growth. But despite great progress, society still faces complex problems that are interconnected and often universal. They include COVID-19, the climate emergency, biodiversity loss, inequality, social exclusion and declining trust. (16) This report explores some of these further in its fourth section.

The Future of the Corporation programme was set up to ask the question “what is the role of business in society?” It demonstrated in its 2018 research that the answer to this question is not merely to maximise returns for shareholders (17), as has conventionally been suggested, because this narrow view of business has often led to poor outcomes for society. While many businesses have been a major force for good (18), examples abound stretching back over decades and centuries of those that have caused immense detriments. (19)

Business can and does do more than maximise returns for shareholders. Based on extensive academic research and engagement with business leaders, politicians, investors and civil society experts, we have concluded that the social responsibility of business should not merely be to increase its profits, but rather:

to create profitable solutions for the problems of people and planet, while not profiting from creating problems for either.

This is the vision to which this report seeks to give effect and, crucially, it is one that business supports. (20) This raison d’être for business embraces its potential to be a source of solutions to society’s problems, not the causes of the problems. In a world where solving problems is the primary purpose of business, it naturally works with others to find solutions for customers and communities, employees and the environment, societies and suppliers in ways that are commercially viable, financially sustainable and profitable. Still more fundamentally, it does not profit from creating problems because that is an illegitimate source of profits, which should be reflected in the way in which profits are defined and measured.

There are examples of businesses of all sizes that advocate this vision. We refer to some in this report and there are many more, including a growing number of “B Corps” (that commit themselves to purpose), social enterprises and businesses incorporated under rules that enable a focus on purpose – such as public benefit corporations in the US, and entreprises à mission in France. But they all have their limitations, and they have not to date brought about the transformation that is sought. (21)

Our work within this programme has brought together an evidence base to show that redefining the purpose of business is a straightforward, effective and powerful way of improving the performance of companies and economies as well as enhancing personal, social and environmental wellbeing for current and future generations. (22) The change corrects a fundamental flaw in the functioning of markets and competition, and it promotes a race to the top not the bottom that rewards solutions not problems.

Proposals: how to make the shift?

This section of the report brings together the Future of the Corporation findings over the past four years, further refined and reviewed in our 2020 policy labs and through continuous and ongoing engagement with our stakeholder networks (23), and presented as a series of policy and practice proposals which describe how to shift from the current situation to the future described by the vision above.

The public policies and business practices are set out below, giving business leaders and policymakers guidance and illustrative examples of what can be done to make the shift to purposeful businesses. It is not a toolkit, nor a step-by-step guide, but an illustration of how to formulate proposals around the eight principles of purposeful business on law and regulation, ownership and governance, measurement and performance, and finance and investment. It is not intended to be country-specific. Although we consider how it applies to the UK, we hope others will conduct similar analyses in other jurisdictions, considering their specific contexts and adjusting the approach accordingly.

Most significantly, we emphasize that no single lever nor institution can deliver this change alone. Comprehensive reform involves a coherent set of policies and practices to be adopted by government, regulators, business and investors. Systemic change needs systematic solutions. Though the policy and practice proposals are presented in turn, they should be viewed as a collective whole.

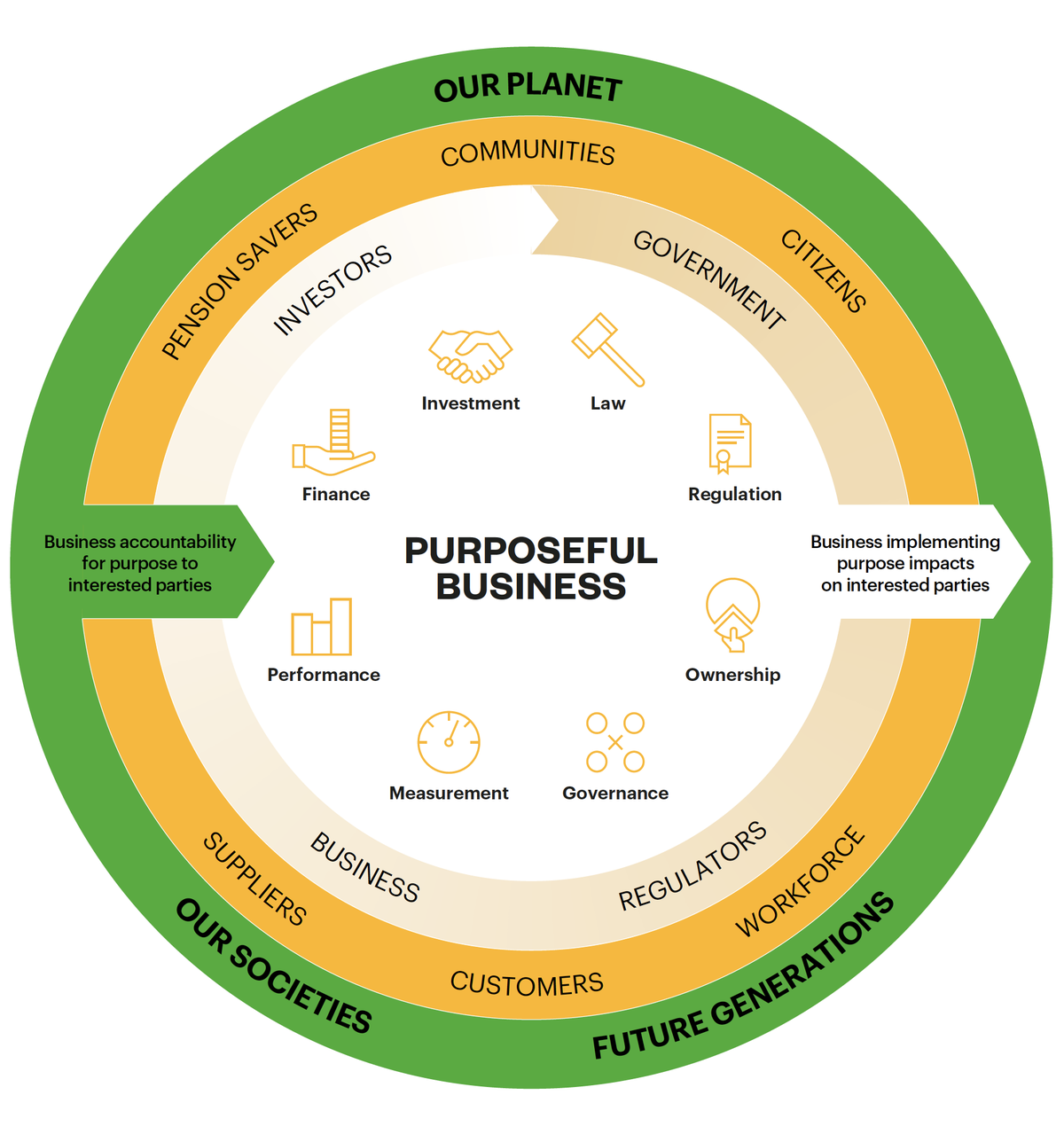

There is one pre-requisite to enable and encourage purposeful business in such a systematic way: a supportive legal, regulatory, governance and reporting framework. Such a framework is a necessary but not sufficient condition to bring about a shift to purposeful business, so we have also described two mechanisms that use the framework to deliver coherent reform:

- Accountability: using the legal, regulatory, governance and reporting framework to hold companies to account for complying with corporate purposes of profitably solving problems of people and planet and not profiting from creating them; and,

- Implementation: ownership, measurement, finance, innovation and investment through which people harness the potential of markets to deliver profitable solutions which benefit customers, the workforce, investors, communities, society and the environment.

Figure 1: Using accountability and implementation mechanisms to put purpose at the heart of business.

The UK provides a particularly clear illustration of the distinction between these two mechanisms. In terms of the pre-requisite for a supportive environment, the UK has adopted legal, regulatory, governance and reporting rules that accommodate purposeful business, although they do not actively encourage it. (24) But UK regulators do not yet have the powers to hold directors sufficiently to account for fulfilling their purposes. (25) The framework itself is a necessary, but not sufficient condition.

Exercising the option within UK company law to adopt purposes that go beyond promoting shareholder value is uncommon, and interests of employees, suppliers, consumers and other stakeholders therefore remain derivative of those of shareholders. There is insufficient appreciation on the part of directors of their duties under the law to respect the interests of their stakeholders in promoting the success of companies for the benefit of their shareholders over the long term. (26)

The UK corporate governance code goes well beyond the law in emphasising the importance of corporate purpose, and requires boards of companies to determine their purposes and ensure that their values, strategy, and culture are aligned with them. However, here too accountability and compliance have been deficient. (27) In relation to both law and corporate governance, accountability needs to be strengthened internally within organisations and externally by regulators.

Policy and practice illustrations

Throughout this section, two types of illustrations are used, both described as starting points that show a range of business policies and practices at different stages of implementation. The business practice starting points are only a small selection of what is happening at present and many more have been cited elsewhere. (28) The report is not endorsing any of the examples or businesses featured, and where the policy starting points are linked to a particular organisation, we encourage further engagement with that organisation or initiative to examine them in detail. (29)

But as the Future of the Corporation research and previous reports have demonstrated, purposeful business is more than accountability and compliance with law, regulation, governance and reporting. It is about the values, commitment, culture and cooperation of people that help implement corporate purposes that solve the problems of people and planet through strong ownership and inspiring leadership; building close relations between institutions and companies to finance entrepreneurship, innovation and investment in purposeful businesses; putting purpose at the heart of companies’ measurement, valuations and incentives; and building common purpose between business and government actors to solve local, national and global challenges. (30)

The UK business environment reveals deficiencies in implementation as well as accountability. It does not for the most part have the long-term holders of significant blocks of shares who can commit to promoting the successful implementation of corporate purpose which are commonplace in even the largest listed companies in most countries around the world. (31) Long-term relationships among providers of risk capital at local levels are critical to funding the start-up and growth of small and medium-sized enterprises, but are largely absent outside of London and the South-East of the UK. (32)

In addition, other countries have been more successful than the UK in building partnerships between business and government to co-invest in common purposes of tackling local, national and international policy issues. (33) These observations highlight the failure of the UK to use market levers to incentivise commitment, culture and cooperation around corporate purposes.

Finally, measurement is an area where complementary reform is required at an international level in order to support change on a national level, including in the UK. Several international initiatives are currently in progress to ensure that companies and investors have reliable systems of measuring environmental and social impacts but to date they have not focused on measuring, valuing and incentivising corporate purpose. (34)

The proposals that follow and that are collated in the summary table overleaf establish the accountability and implementation mechanisms required to ensure that the UK’s relatively and already well-formed set of ‘rules’ enable and encourage purposeful businesses to prosper. Similar analyses can be undertaken elsewhere to identify and rectify gaps in accountability and implementation for delivering purposeful businesses in countries around the world.

Summary of proposals under the eight principles for purposeful business

1: Company law

Governments put purpose at the heart of company law and the fiduciary responsibility of directors.

More specifically it is proposed that:

- Company law emphasises duties of directors to determine and implement company purposes.

- Governments publish guidance on how companies can incorporate purpose in their legal form, for example in their articles of association.

2: Regulation

Regulators are given new powers to hold directors and controlling owners to account for their corporate purposes

Regulators responsible for particular business sectors that provide public functions require utilities, banks, and other licensed companies they oversee to adopt purposes which align with their public interests and engage with their stakeholders about them.

More specifically it is proposed that:

- A new duty is placed into the mandate of all regulators to enforce the principle that companies do not profit from failing to meet the minimum standards that the regulator sets, where those standards are ideally principles- based.

- Regulators responsible for directors use their powers to engage with stakeholders on the conduct of directors.

- Regulators responsible for particular business sectors that provide public functions promote meaningful engagement and consultation between regulated companies and relevant stakeholder groups to align those companies’ purposes with public interests.

3: Ownership & 4: Governance

Companies place purpose at the heart of their annual reporting and demonstrate to their stakeholders how their ownership, governance, strategy, values, cultures, engagement, measurement, incentives, financing and resource allocation deliver it.

Investors engage with companies about the nature and implementation of their purposes.

Regulators address impediments that may exist to companies having long-term committed shareholders.

Companies identify long-term committed holders of blocks of their shares. They develop internal values, cultures and systems of measurement and incentives that encourage embedded ownership of purpose throughout their organisations.

More specifically it is proposed that:

- Owners, boards and executives take responsibility for overseeing the adoption and implementation of corporate purposes.

- A company board: (a) ensures that the company’s values, culture and strategy are aligned with the implementation of its purpose; (b) is accountable to the company’s shareholders, employees and other stakeholders involved in the implementation of its purpose; (c) reports to the company’s shareholders and stakeholders on the resourcing, measurement and performance of its activities against its purpose; (d) ensures that the company’s incentives and remuneration are based on fulfilment of its purpose; and (e) encourages embedded ownership of purpose throughout their organisations.

- Investment law ensures that the owners of shares in a company support and promote stewardship and the long-term fulfilment of its purpose.

- A review is undertaken of the regulatory impediments that may exist to committed long-term shareholders.

5: Measurement & 6: Performance

Investors promote measurement and reporting of company purposes and ensure that required systems of data and information are available to evaluate company performance against purpose.

Investors evaluate companies’ performance and future prospects against their purposes.

Regulators and international standard setters promote systems of measurement and accounting for company purposes and ensure that financial reports reflect profits and costs of delivering them.

More specifically it is proposed that:

- International standard setters define baseline metrics that apply universally to all companies, allowing for additional company-specific metrics.

- Each company determines metrics that fulfil and evaluate its purpose and ensures that those metrics measure: (a) the inputs and outputs that companies use and produce; (b) the outcomes of their activities; and where feasible to measure, (c) the impacts they have on other parties.

- Companies account for the resources required to deliver their purposes, and determine their profits, performance, and internal incentives accordingly.

- Investors and other interested parties evaluate a company’s performance according to both financial and non-financial impacts of its activities.

7: Finance & 8: Investment

Investors develop the expertise required to support long-term financing of small, local as well as large, global purposeful businesses.

Governments, companies, and non-governmental organisations co-invest in partnerships based on common purpose around tackling issues such as inequality, social exclusion, climate change, biodiversity loss and the future of work.

More specifically it is proposed that:

- Companies ensure that they have the long-term risk-sharing equity that is required to fulfil their purposes.

- Public and private finance adopt a place-based approach to the start-up, scale-up and training of new and growing enterprises, and SMEs.

- Financial institutions steward investments in companies to promote companies’ purposes.

- Companies partner with other organisations in public, not-for-profit as well as commercial sectors in investing in common purposes.

- Fiscal and monetary policies promote financing and investment in common purposes.

- Public and private sectors invest in training, educating and re-skilling employees at all levels of organisations to fulfil their common purposes.

Company law

This subsection considers the role of company law in establishing accountability for corporate purposes, paying particular attention to the duties of directors.

Present situation

Company law in the UK requires directors to promote the success of the company for the benefit of its shareholders, having due regard to the long term and the interests of other stakeholders. (35)

Nature of the problem

In the UK and countries with similar systems, the law requires that directors promote the interests of shareholders (‘shareholder primacy’) and those of other stakeholders only to the extent that they enhance long-term shareholder value (‘enlightened shareholder value’). They should not promote the interests of other stakeholders in their own right. (36) This view subordinates the interests of most stakeholders to those of shareholders, even in the long term.

The debate of shareholder versus stakeholder has dominated discussion of company law for decades, without much advancement. (37) But it is a sterile debate, and misses the point. The issue is not whether to promote the interests of shareholders or stakeholders but how to do both by profitably solving problems of people and planet. It shifts the focus of the firm from any particular interest group to doing what we want it to do – solve problems profitably.

Evidence and insight from the Future of the Corporation programme’s engagement processes have consistently shown that company law is often interpreted as being permissive of multiple corporate objectives, and it is claimed that it is possible for companies to adopt purposes beyond a narrow interpretation of shareholder interests. However, the ambiguity is problematic for directors wishing to pursue purposes other than those focused on financial goals. It leaves their organisations exposed to predators – hedge fund activists and hostile bidders – seeking to enhance short-term value over other objectives. (38) It undermines the functioning of markets by allowing companies that profit from creating detriments to drive out those that do not. The law currently provides no protection against such conduct.

Policy and practice proposals

Governments put purpose at the heart of company law and the fiduciary responsibility of directors.

More specifically it is proposed that:

- Company law emphasises duties of directors to determine and implement company purposes.

- Governments publish guidance on how companies can incorporate purpose in their legal form, for example in their articles of association.

Collectively, these proposals will support the development of an operating environment that enables and encourages purposeful business. As Future of the Corporation research and others like the FRC have set out previously, corporate purpose is the reason for the creation and existence of a company, and UK company law should therefore be reformed so it is the basis of the laws that establish the company. (39) One example that is gathering support and is attuned to this is the Better Business Act, as highlighted below.

Policy starting points: Changing Section 172 of the Companies Act to require companies to state their purpose in their articles of association.

Illustrations, examples and recent developments

Possible wording for such an amendment is included in the “Better Business Act” proposed by B Lab UK and supported by 0ver 650 businesses and the Institute of Directors. Legislation would require companies to adopt purposes that aim to benefit people and planet as well as shareholders, and report on their success in so doing. (40)

Possible roles for different system actors

- Government: lead

- Business (boards and management): adopt and input

- Shareholders: support

But the necessary legislative reform may be a complex and drawn-out process. In the interim, there are measures that can be taken rapidly within the context of existing law to encourage and support the adoption of corporate purposes. For example, guidance and pro-active government support and leadership would bring clarity to what is intended of the law and assist companies in determining how they can adopt purposes.

Policy starting points: Interim measures to use model articles to encourage business to embed purpose

llustrations, examples and recent developments

Future of the Corporation policy labs have highlighted the value of detailed case studies aiming to raise awareness of the benefits and performance of purpose-driven businesses. Additionally, model articles would provide templates for how shareholders can mandate directors to deliver the company’s purpose and integrate other stakeholder interests. This would represent not just a statement of purpose but also a commitment to its fulfilment, requiring agreement from shareholders for their adoption and amendment. (41)

Possible roles for different system actors

- Government: lead

- Business (boards): adopt

- Shareholders: support

The Companies Act (2006) currently permits companies to pursue “purposes other than the benefit of its members” (shareholders) in Section 172(2). (42) There is therefore already provision for inclusion of company purpose in UK law and this could become the norm that is expected of most firms, particularly where they are seeking government contracts or provide public services and infrastructure. (43) In certain circumstances, the Public Services (Social Value) Act (2012) already enables public bodies to make such requirements and this is discussed at more length under Finance and Investment below. (44)

Policy starting points: Interim measures to use explanatory guidance to encourage use of existing option to embed purpose

Illustrations, examples and recent developments

Future of the Corporation policy labs highlighted that explanatory guidance to section 172(2) of the 2006 Companies Act, could be readily updated to encourage businesses to use the existing legislation to embed purpose. The explanatory guidance currently suggests that this paragraph is intended for charities or community interest companies, but it does not exclude the possibility of other companies using it. (45) The guidance should be used to encourage all businesses stating a purpose to use this existing legislation to make a commitment to their purpose in their articles of association.

Possible roles for different system actors

- Government: lead

- Business (boards): adopt

- Shareholders: support

Practice starting points: Embedding purpose in articles of association

B Corps are for-profit businesses that make a legal commitment to purpose. Neighbourly is a small B Corp which has stated its purpose in its Articles as follows: “The purposes of the Company are to promote the success of the Company for the benefit of its members as a whole and, through its business and operations, to have a material positive impact on society and the environment, taken as a whole.” (46) CEO of Neighbourly, Steve Butterworth, describes Neighbourly as being, “a platform designed to help a corporate business activate its social purpose at a local level, but at scale”. Neighbourly’s business model uses licence and transaction fees from corporate clients, enabling free access to the platform for community groups. It has helped corporations donate nearly £14 million, 72 thousand volunteer hours, and over 56 million meals since it was launched in 2012. (47)

Larger businesses have been less likely to mirror this practice, but Anglian Water, a regional British water utility which was referred to in the previous Future of the Corporation report is one example. (48) Commenting on the challenges this has presented, Andrew Brown, Head of Sustainability, mentions the reasons the company went down this route:

“There is a difference between writing a purpose statement and slapping that into your annual report and accounts, and actually embedding a purpose in your business. That’s one thing we are attempting to do, and have formally done with our articles of association

… [Then] unless we lock it in and demonstrate that we are genuinely willing to create this purpose, people could always think that we are just spinning a good story … [Finally], what happens if we we’re bought out by other investors, and they take a completely different approach? … It’s also a signal to other investors who might be interested in us as a company, that this is what we do. This is what we believe in. You can’t buy us out and change this purpose. You have to buy into this purpose.”.

Regulation

This subsection considers the role, mandate and approaches taken by regulators in enforcing accountability by directors, and the specific role that sector regulators play in enhancing mechanisms of implementation by licensed companies.

Present situation

The current model of regulation towards directors is centred around duties that relate to commercial, employment, consumer, environmental, human rights and investor-protection laws. Alongside this, specific rules apply to regulated and licensed companies in sectors that provide public functions, such as utilities, financial institutions and auditors.

Nature of the problem

The prevailing model of regulation of company directors does not make them accountable for the corporate purpose. (49) This is a problem not only of the rules themselves (discussed in the company law section above), but also of the role, mandate and approaches taken by regulators charged with their enforcement.

Purpose can be enforced by both public and private mechanisms. Private mechanisms include the current mechanisms by which shareholders are able to hold directors to account under company law, including by exercising powers to appoint directors, passing resolutions to direct the board and, in extremis, removing directors or pursuing directors for breach of duty. Regulation currently lacks the necessary powers to hold companies to account for their purposes through public mechanisms. As a result, enforcement agencies and courts of law impose fines and penalties to hold business in check and promote conduct that is consistent with social objectives, but this can fail to prevent harmful practices, (50) and results in a lag when innovative technologies like social media create rapid change. (51)

The role, mandate and approach of regulators is undermined in this regard by the divergence of interests that can exist between companies focused on maximising shareholder value and regulators promoting public interests. Future of the Corporation research has highlighted the value of alignment of purposes and the importance of culture and values when it comes to implementation; (52) even when rules are clear, compliance varies according to behavioural psychology, values and economic and cultural incentives. (53)

Policy and practice proposals

Regulators are given new powers to hold directors and controlling owners to account for their corporate purposes.

Regulators responsible for particular business sectors that provide public functions require utilities, banks, and other licensed companies they oversee to adopt purposes which align with their public interests and engage with their stakeholders about them.

More specifically it is proposed that:

- A new duty is placed into the mandate of all regulators to enforce the principle that companies do not profit from failing to meet the minimum standards that the regulator sets, where those standards are ideally principles-based.

- Regulators responsible for directors use their powers to engage with stakeholders on the conduct of directors.

- Regulators responsible for particular business sectors that provide public functions promote meaningful engagement and consultation between regulated companies and relevant stakeholder groups to align those companies’ purposes with public interests.

These proposals create specific accountability for corporate purposes by establishing institutions with the capability and powers to hold directors to account, alongside implementation mechanisms to engage stakeholders in the process. These powers could include, for example, the power to conduct market studies and investigations, the power to investigate complaints from stakeholders, the power to issue warning or fines where purposes have clearly been breached and the power to make recommendations to other regulators.

At the sector-level, the focus is on alignment between corporate purposes and public interests, based on meaningful engagement with stakeholders. More broadly, all regulators would need to uphold the principle that companies do not profit from failing to meet the minimum standards that the regulator has set. Taken together these proposals align with other developments towards a principles-based approach to regulation.

Policy starting points: Purpose as a basis for meaningful engagement between regulators and regulated companies

Illustrations, examples and recent developments

Sustainability First highlights the need for regulators to adopt longer-term, forward-looking perspectives which use purpose to embrace wider citizen as well as consumer interests and encourage partnerships and collaboration. Sustainability First has also called for a new process of ‘adaptive planning’ in utilities like energy and water, with future thinking and scenarios at the heart of infrastructure investments delivering over multiple price- control periods. They state that in monopolies, intergenerational issues and pathways to net zero and adaptation cannot be conducted principally through five-year price reviews, which can incentivise companies to delay difficult decisions and preclude long-term strategic investment. (54) More broadly, growing interest in deliberative engagement methodologies such as citizens assemblies (55) presents further opportunities for meaningful engagement linking public interests to corporate purpose.

Possible roles for different system actors

- Government: lead

- Business: adopt and support

- Shareholders: support

An extensive literature (56), supported by engagement through Future of the Corporation roundtables in earlier phases and the policy labs over the past year, has highlighted both the importance and limitations of regulatory systems in influencing corporate behaviour. The focus of the proposals presented here on high-level principles around alignment on purpose aims to balance these factors and enable regulators to determine a set of required outcomes based on accountability and meaningful engagement, while leaving space for companies to innovate.

Extensive research exploring culture, law and regulation (57), highlights the importance of these mechanisms of collaboration, consultation with interested parties, a forward- looking approach and accountability. It also emphasizes the range of interested parties that could be given consideration, for example: workers, communities, citizens, future generations, pension savers, suppliers, environmental representatives, and of course, shareholders. Like companies, regulators must identify their stakeholders, consult them, and determine and commit to their purpose (as described in the next section, considering governance).

Practice starting points: Collaborative approaches to regulation, public services and customer welfare

Collaboration between regulators, communities, government and companies is illustrated by Thriving Communities Partnership (TCP), a member-funded cross-sector collaboration hosted by Yarra Valley Water, Melbourne’s largest water utility company. TCP aims to ensure that everybody has fair access to the modern essential services they need, including utilities, financial services, telecommunications and transport. It places human interests at the centre of everything they do, aiming to build more resilient communities and stronger businesses, bringing together over 170 organisations from ASX listed companies, government and regulation, and the community sector to solve critical social problems in partnership. (58)

Practice starting points: Biodiversity offsetting to avoid profiting from creating problems

Some sectors face more challenges than others in avoiding profiting from problems. Mining is an example of a sector that provides vital resources for modern essentials like smartphones but has frequently failed to protect people and planet in the process. Anglo-American illustrates some of the new types of initiatives in mining to address these issues. Its stated purpose, “re-imagining mining to improve people’s lives” led it to seek to tackle the deforestation that results from its operations. For example, between 2014 and 2020, the firm has been investing in “biodiversity offsets” in the Minas Rio area by acquiring over 6,000 hectares of offset sites. Since first acquiring the land, Anglo has invested $3.5 million in the conservation of the 12,000 hectares that they manage, and another $6.4 million into the restoration of a separate 1,300 hectares in the area. A further $2.4 million was invested for monitoring the fauna in the areas, and $2.8 million was donated to reforestation of native trees in previously damaged areas. (59) Evaluating whether this initiative delivers a net zero or better impact on biodiversity is exactly why the accountability mechanisms proposed in this report are needed.

Ownership and governance

This subsection considers the responsibilities of owners, boards and executives in implementing corporate purpose; how they are all accountable to shareholders, the workforce, customers, communities and other stakeholders through governance; and the value of supporting leadership and culture. The types of financing and role of investment in funding innovation are considered under Finance and Investment.

Present situation

Most prevailing concepts of corporate ownership derive from a historic property-right view of the firm that, as investors and residual claimants, shareholders own firms. (60) Under this system, investors are owners with rights of control over the firm, in particular in relation to the appointment and removal of members of the board of directors.

Owning shares has certain features associated with it, including a claim on dividend distributions, a right to sell shares, and a right to vote on some propositions regarding the operation of the firm, including the appointment and removal of directors. It is the board of the firm that has control over the firm and the board delegates that responsibility to the executive who in turn employ managers to run the business.

Nature of the problem

Shareholders do not own firms in the way in which a property-right view of the firm would suggest. They own a share in a firm which confers certain rights, including the approval and removal of directors. Boards are thereby predominantly held to account for meeting financial goals in the interests of shareholders. In contrast, a purpose-led view of the firm requires that directors be held to account for implementing the company’s purpose. (61)

In the presence of widely dispersed shareholders, accountability of directors to shareholders is weak. Shareholders often fail to exercise their voting rights, particularly on non-financial resolutions. (62) Shareholders may be driven by a short-term outlook (63), and activist shareholders, purchasing blocks of shares and forcing changes to strategy (64), might have the effect of focusing the attention of boards on short-term share-price performance, irrespective of their stated purpose. (65)

Recent rule changes such as the 2018 Corporate Governance Code are beginning to alter this. The 2018 UK Corporate Governance Code defines the responsibility of the board to be to “establish the company’s purpose, values and strategy, and satisfy itself that these and its culture are aligned.” (66) Boards must therefore determine the company’s purpose, engage meaningfully with employees, communities, suppliers and other stakeholders and consider the impact of the company on the environment and society. (67) But, as a recent assessment by the Financial Reporting Council (the FRC) suggests, boards often do not possess the necessary skills, knowledge, experience, and motivation to discharge those duties. (68)

Policy and practice proposals

Companies place purpose at the heart of their annual reporting and demonstrate to their stakeholders how their ownership, governance, strategy, values, cultures, engagement, measurement, incentives, financing and resource allocation deliver it.

Investors engage with companies about the nature and implementation of their purposes.

Regulators address impediments that may exist to companies having long-term committed shareholders.

Companies identify long-term committed holders of blocks of their shares. They develop internal values, cultures and systems of measurement and incentives that encourage embedded ownership of purpose throughout their organisations.

More specifically it is proposed that:

- Owners, boards and executives take responsibility for overseeing the adoption and implementation of corporate purposes.

- A company board: (a) ensures that the company’s values, culture and strategy are aligned with the implementation of its purpose; (b) is accountable to the company’s shareholders, workforce and other stakeholders involved in the implementation of its purpose; (c) reports to the company’s shareholders and stakeholders on the resourcing, measurement and performance of its activities against its purpose; (d) ensures that the company’s incentives and remuneration are based on fulfilment of its purpose; and (e) encourages embedded ownership of purpose throughout its organisations.

- Investment law ensures that the owners of shares in a company support and promote stewardship and the long-term fulfilment of its purpose.

- A review is undertaken of the regulatory impediments that may exist to committed long-term shareholders.

The logic behind these proposals is that in order to implement a company’s purpose, there needs to be clear responsibility and accountability for it, and the formulation and determination of a company’s strategy in fulfilment of its purpose should be overseen and involve those who are most significant in its implementation.

When a company is established, the founder naturally holds this responsibility, defining and promoting its purpose. Where founders pass on and sell their shares in substantial blocks to members of their families, private equity investors or other companies, then these groups of block shareholders share that responsibility and accountability. Where shares are widely dispersed on stock markets, the board of directors have responsibility and accountability for overseeing the company’s purpose, and the process of appointment, appraisal, reward and removal of directors should be directed towards the implementation and ongoing development of its purpose. The board and the executive should also be guided by the purpose as the determinant of the firm’s strategy and culture, and the basis on which resources are allocated and performance measured throughout the organisation.

Policy starting points: Clarifying the role of the board in corporate governance

Illustrations, examples and recent developments

The UK Corporate Governance Code 2018 goes further than any other at present in describing the governance of purpose. Principle B states that:

“The board should establish the company’s purpose, values and strategy, and satisfy itself that these and its culture are aligned. All directors must act with integrity, lead by example and promote the desired culture.” Principle C then states that: “The board should ensure that the necessary resources are in place for the company to meet its objectives and measure performance against them.”

This describes well what should be expected of the governance of a firm. The board should determine its purpose, ensure that it is core to the business, not just marketing or promotion, and be the overarching determinant of its strategy. The board should ensure that the company’s values and culture are aligned with it, that the necessary resources and investment are provided to fulfil it, and that its performance is measured against it.

Possible roles for different system actors

- Regulators (FRC): monitor

- Business: implement in full

In addition, while responsibility and accountability for a corporate purpose may reside with the board, it is the role of the executive to ensure that implementation does not just sit at the top of an organisation. The purpose is determined and if necessary, changed, by engagement throughout the organisation and realised through adoption by every part of it.

This is because achievement of purpose requires a sense of ownership by everyone in the organisation, not just those with formal rights and responsibilities for it and those at the top, but throughout from the board to the shop floor. Shareholders, as providers of finance and bearers of financial risk, have an important role to play in this, but so too do other stakeholders – workers, in particular.

Corporate governance should therefore be designed to promote a common sense of purpose amongst all those involved in and affected by its implementation, including those who use and rely on its goods and services. Future of the Corporation policy labs and roundtables have highlighted that all of these stakeholders should be an integral part of corporate governance. (69)

As also highlighted by previous Future of the Corporation reports, establishing this sense of ownership of purpose will require innovations in governance practices. Workers on boards and two-tier board structures are commonplace in some countries. (70) The corporation of the future may choose to use citizens assemblies, social media, big data and other emerging techniques to encourage participation and engagement. One benefit from these engagements will be a greater diversity in the skills, experience and backgrounds of boards, better equipping them to oversee the implementation of corporate purpose. (71) Meanwhile, engagement is also highlighted in the Regulation section above as it is a key mechanism to align corporate purposes with public interests.

Practice starting points: Varied stakeholder engagement strategies

Examples are emerging of wide-ranging engagement strategies being adopted by companies seeking to involve diverse groups of stakeholders. SSE plc is a UK energy producer. Its purpose is to provide energy needed today while building a better world of energy for tomorrow. It has a varied approach to stakeholder engagement, identifying six groups: employees; shareholders and debt providers; energy customers; government and regulators; NGOs, communities and civil society; and supplier, contractors and partners. Each is targeted by a range of engagement methods and reporting highlights issues raised and value created. (72) Unilever is a global consumer goods company. Its purpose is to make sustainable living commonplace. It also adopts a varied approach to engagement, based on an annual materiality assessment. It states that its stakeholders are governments, NGOs, suppliers, customers, consumers, scientists, communities, peer companies and trade associations. (73)

Policy starting points: Defining and implementing purpose

Illustrations, examples and recent developments

The Enacting Purpose Initiative has set out a framework entitled ‘SCORE’ for boards to articulate and implement purpose within their organisations: (74)

Simplify: make your purpose simple and convincing, with shared frames of reference. Complicated strategies fail.

Connect: once it has been simply and clearly articulated, corporate purpose must drive what the organisation does – its strategy and capital allocation decisions.

Own: ownership of purpose starts with the board. It has to put in place appropriate structures, control systems and processes for enacting purpose.

Reward: the board has to define measures of performance that evaluate the success of the organisation in delivering on its purpose.

Exemplify: a key role of leadership is to bring organisational purpose to life through communication and narrative strategies.

Possible roles for different system actors

- Business (boards): lead and oversee

- Business (management and all employees): adopt and input

- Shareholders: endorse and support

Finally, Future of the Corporation research and engagement has consistently highlighted the importance of corporate culture for enabling purposeful business. (75) The board has the responsibility to ensure consistency of the values and culture of the organisation, not just with its purpose (76) but with all aspects of its management, measurement and reward (see Measurement and Performance section below) that complement implementation of its purpose.

Practice starting points: Establishing responsibility for purpose

Global companies can struggle with a legacy of issues that cannot be addressed simply by a purpose statement. Establishing responsibility for purpose throughout a company is crucial, and every company on this journey will need to establish its own supportive culture. BT Group plc offers an illustration of a company engaged in this process. The starting point was the board: its responsibilities set out in the 2021 annual report are to establish the group’s newly articulated purpose. One of the board’s six strategy committees, its Digital Impact & Sustainability Committee, is directly charged with ensuring that the purpose is pursued. (77) The firm also established a Colleague Board, consisting of 10 members representing the firm’s business units, which provides feedback on board activity. In 2021, the Colleague Board gave advice to the chief executive regarding the company’s previous and newly articulated purpose. The group established a ‘Purpose for Business Team’ tasked with integrating the purpose throughout the organisation and helping everyone in the company connect their work to the purpose of the organisation.

Measurement & performance

This subsection considers the role of metrics and reporting that enable investors and other stakeholders to evaluate and account for the performance of the company in implementing its corporate purpose.

Present situation

Measurement is conventionally undertaken in relation to the financial performance of the firm. It focuses on the tangible assets of a company – its buildings, land, plant and machinery – and its financial assets and liabilities. Recently, there has been a proliferation of measures around Environment, Social and Governance (ESG) considerations. These are particularly concerned with factors that are material to investors and other stakeholders, and, in many cases, they take the UN Sustainable Development Goals as their starting point.

Several international and national bodies are involved in these initiatives. The European Commission is developing its non-financial reporting directive; the International Financial Reporting Standards (IFRS) Foundation is proposing an International Sustainability Standards Board; and the UK government is committing to mandating the Taskforce on Finance-Related Climate Disclosures. (78)

Nature of the problem

The axiom ‘you manage what you measure’ has great salience in business, and insights from the programme’s engagement with senior business leaders have consistently highlighted the critical importance of measurement. But what to measure, how to measure it, how to report it, and how to use data to evaluate performance have all been the subject of active debate. (79)

Despite recent progress, there remains little consistency, comparability or correlation between different ESG measures. (80) There is little data assurance, verifiability or auditing of information, and there is therefore concern about its reliability or relevance to delivery of better outcomes. There is also considerable confusion between ESG and measurement of purpose. (81)

Meanwhile, accounting systems remain focused on the financial bottom line, and valuations are predominantly restricted to future financial earnings. Nowhere is a company required to account for the total costs that it incurs or should incur in avoiding or rectifying the problems it inflicts on society or the planet. (82) Evaluation of non-financial performance is challenging and may require a broader range of techniques, including qualitative approaches, than has been the case to date.

Policy and practice proposals

Investors promote measurement and reporting of company purposes and ensure that required systems of data and information are available to evaluate company performance against purpose.

Investors evaluate companies’ performance and future prospects against their purposes.

Regulators and international standard setters promote systems of measurement and accounting for company purposes and ensure that financial reports reflect profits and costs of delivering them.

More specifically it is proposed that:

- International standard setters define baseline metrics that apply universally to all companies, allowing for additional company-specific metrics.

- Each company determines metrics that fulfil and evaluate its purpose, and ensures that those metrics measure: (a) the inputs and outputs that the company uses and produces; (b) the outcomes of its activities; and (c) the impacts they have on other parties.

- Companies account for the resources required to deliver their purposes, and determine their profits, performance, and internal incentives accordingly.

- Investors and other interested parties evaluate a company’s performance according to both the financial and non-financial impacts of its activities.

Future of the Corporation research and engagement has found that companies should move away from the narrow measurement of financial performance to a broader approach, where purpose should be the driver of companies’ measurement systems. Metrics that are relevant to purpose should enable evaluation of both the resources that are required to deliver purpose and the criteria by which success in achieving it can be assessed. Since measurement forms the basis of internal management accounting and external reporting, appropriate metrics are critical to ensuring accountability for purpose and to aligning the interests of companies’ investors, workers, suppliers and other stakeholders with their purposes. (83)

The responsibility of a company does not stop at the proverbial factory gate, with inputs used in its operations or outputs produced by them. It extends to the effect that both inputs and outputs have on people, communities, societies, and the natural world. Standards setters will therefore play a key role in ensuring that the metrics a company chooses are not restricted to its inputs and outputs but extend to its outcomes the changes brought about by the firm – and their impact on the wellbeing of others. (84) In particular, they establish whether changes caused by a firm’s activities confer benefits or detriments on other stakeholders.

Policy starting points: Emerging standards and methodologies for measuring purpose

Illustrations, examples and recent developments

Significant strides have been made towards changing expectations and standards on non-financial disclosures, both in the UK and globally, particularly in relation to sustainability reporting and ESG indices. (85) The International Financial Reporting Standards foundation (IFRS), which sets standards currently in more than 140 jurisdictions, is working towards establishing an international sustainability reporting standards board. (86) A merger between SASB and IIRC has taken place (87) and the UK has recently committed to align with TCFD and SASB recommendations. (88)

Nevertheless, Future of the Corporation engagement has highlighted that it is necessary to give greater regard to the ‘S’ (social) of ESG – that is, to people, alongside the ‘E’ (environment). Measurement according to purpose helps to achieve this integration and should be considered alongside sustainability reporting.

Possible roles for different system actors

- Standard setters: lead

- Business (boards, management and all employees): adopt and input

- Shareholders: endorse and support

Accounting systems and associated systems of valuation must reflect this principle of extending measurement from inputs and outputs to outcomes and impacts. Doing so will enable a company to establish the resources it requires to fulfil its purpose. An accounting system that does this will enable each company to determine and expend the costs of rectifying the problems it creates, so as not to profit from them and to sustain the resources on which it depends for its activities. (89) The result will be determination of companies’ profits which reflect the earnings they derive from delivering solutions to problems of people and planet without causing problems for others – that is, their purposes.

Policy starting points: Initiatives to develop accounting for purpose

Illustrations, examples and recent developments

The Impact-Weighted Accounts project is aiming to create accounting statements that transparently capture external impacts in a way that drives investor and managerial decision making. (90)

Integrated reporting should directly link purpose to financial as well as social, environmental and other external impacts, with the full spectrum of a company’s stakeholders involved in the process.

Possible roles for different system actors

- Government, regulators and standard setters: lead

- Business (boards, management and all employees): adopt and input

- Shareholders: endorse and support

With metrics that enable performance and profits to be expressed in these terms, companies’ internal policies will become better informed regarding remuneration, board strategy, internal management, external reporting, investor stewardship and stakeholder engagement. In this way, the measurement system allows executives and workers in an organisation to relate their activities, the resources they require and the investments they make to the company’s purpose and strategy. It is, therefore, vital to the implementation of a system of purposeful business. For example, executive pay remains an issue that undermines trust; linking a reward structure – remuneration and promotion – to measurement systems reformed in the terms outlined here could help restore confidence that pay reflects success in delivering value to society. (91)

Policy starting points: Encouraging accountability through disclosures on pay, reward and staff satisfaction

Illustrations, examples and recent developments

The High Pay Centre has highlighted that, just as gender pay-gap reporting has prompted a debate about issues such as working hours, workplace culture and the division of labour in the home, the pay-ratio disclosures mandated by the Companies (Miscellaneous Reporting) Regulations in 2018 have helped to focus the debate on executive and low pay. (92) Such disclosures (currently only applicable to listed UK companies) are crucial in allowing shareholders and other stakeholders to assess how far pay policies reflect the purpose of the company and how it values contributions by staff at all levels.

More should be done to involve employees in the reporting process, which could include evidence on employee satisfaction and turnover rates.

Possible roles for different system actors

- Regulators: lead

- Business (boards, management and all employees): adopt and input

- Shareholders: endorse and support

The approach outlined here allows the financial valuations that different parties derive from a company’s activities to be estimated. Although financial valuations are of particular interest to investors and boards, other stakeholders like workers, consumers and communities will be concerned with not only valuations of future earnings but also the benefits conferred on others. For example, policymakers, citizens and philanthropic institutions may wish to determine the value that a company’s activities provide society and the environment, as well as investors. Polling evidence suggests that employees prefer companies with purpose (93) and consumers prefer brands with purpose. (94) A company’s measurement system should therefore provide the basis on which different interested and affected parties can evaluate its performance.

Policy starting points: Reporting on purpose

Illustrations, examples and recent developments

The UK Financial Reporting Council’s (FRC’s) strategic report requirement sets out that company reports should be structured around the company’s purpose, linking it to the business plan, strategy and key performance indicators. (95) The UK government is currently consulting on reforms to the way large companies are held to account for audit and reporting through the establishment of the FRC’s successor body, the Audit, Reporting and Governance Authority (ARGA). (96)